This series is intended principally for someone who has had little if any investment experience. This first Chapter, which is only 5-minutes long, contains all you need to know to start investing. The Chapters that follow have more detailed information for those who want to dig deeper. Start by reading the bullets on the image at right -- it'll tell you where we're going and give you a quick picture of what's in here.

Who should invest? How? When? Everyone should invest. Your money simply won’t grow enough in a savings account to keep up with inflation. Investing allows you to earn more money, even 4 times as much as you can get from the best Certificate of Deposit (CDs). It can be one of the most essential ways to plan for your future. This article from a financial guru and this second article both make it clear that there’s only one thing that will help you build real wealth: you need to invest, and doing it is "deceptively simple".

Investing can be easy, not intimidating. We show you how to do it so it's virtually risk-free, choosing conservative investments that let you sleep soundly at night. Also, I don't recommend that you start by going to a financial advisor; instead, I suggest you read this and then decide whether you need an advisor. Why? Because they don't come cheap and you'll soon learn that you can do as well or better than they can.

But to invest you first need to have funds, so those starting their career need to save, to spend less than they earn. And there are two things you need to do before you start investing:

1. pay off all your credit cards and personal loans, which is critical2, and

2. put away here an emergency fund covering several months of your expenses3.Stocks are the first thing we'll look at, because if held for the long term (5 - 10 years) they perform better than most other investments. For example, the S&P500 index of stocks has had an average annual return of:

11.84% from 1957 to 2024,

15%+ in the 10 years to 10/2025, and

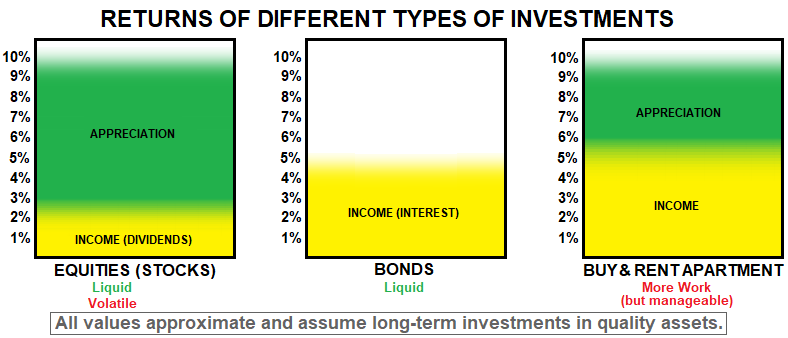

23%+ in the 3 years to the end of 2025.With stocks you're buying partial ownership of one or more companies, and your gains come from the increase in the value of the stocks (appreciation) as the companies grow, but also because many established companies pay a portion of their annual profits, called dividends, to shareholders 4 times a year. Most investors don't buy individual stocks but instead buy a stock mutual fund which buys the stock of many companies, so your money is spread among dozens to hundreds of companies, thereby reducing risk. This achieves one of the principal foundations of investing: diversification. If you have a limited amount of money, why would you buy one stock, or only several? It’s like putting all your eggs in one basket. If that company sputters, you might lose a lot of money.

The stock investment recommended here is the first and perhaps ONLY investment a beginner should make and it's simple: put your money in two different S&P 500 index mutual funds, half in a conventional/traditional S&P 500 index mutual fund and half in an EQUAL-WEIGHT S&P 500 index mutual fund. This departs from my earlier recommendation, and that of other people, to invest only in a conventional/traditional S&P 500 index mutual fund; the reasoning behind this, and suggested mutual funds to buy, may be found here. Also, it’s super easy to start investing — whether it's $100 or $500 or $1,000 every month — it can all be done online without ever leaving your home: you choose an investment firm (I like Fidelity), open an account online, link it to your bank account, choose your investments (like my two S&P500 funds), transfer money online from your bank account to your investment account to start, and then do more transfers over time to add to your investment.

Investments in stock should be with money you won't need for 5 - 10 years. Over those periods, these two index funds have always delivered higher returns than CDs, with no losses and a tax advantage4, plus in 90% of the cases it beats the return of investments picked by experts5 (which is why you can do better than a financial advisor). In the "Stocks" Chapter 2 I also mention other alternatives for investors that are more conservative or more aggressive or want more dividend income, not as a substitute for the two S&P 500 index mutual funds but places where you can put part of your money. It's critical that you then stay the course -- and NOT try to time the market or sell when “experts” are forecasting adverse financial clouds, because that generally leads to very poor performance6.

Bonds are what we'll cover next in Chapter 3. This is where you become a lender and the borrower pays you interest far higher than what you get at a bank. We'll cover the different types of bonds (corporate, government, tax-free municipal). They are suited for those looking for income rather than growth and have historically been used by those who have built a large portfolio of stocks and wished to reduce volatility (i.e., the ups and downs)7.

Real estate is the last investment we'll cover in Chapter 4. Real estate? Yes, because, although it typically requires more funds and it's less liquid (you can't get your money out fast), it can offer income similar to bonds and total returns comparable or superior to stocks without the volatility. In fact, as you can read here, "the most comprehensive analysis of investment returns ever conducted found that residential real estate delivered superior.....returns compared to stocks, with significantly lower volatility".

Other Investments. I don’t cover gold/silver, bitcoin, commodities and other types of investments because I don't know enough about them and I don’t recommend them for beginners. And I strongly urge you to STAY AWAY from get-rich schemes suggested by some -- stick to the investments covered here.

Finally, in the last Chapter 5 that I call "Go Invest", we put all of these concepts together to help you decide what to do, even help you find and assess real estate properties to buy.

While this Chapter 1 may have all you need to invest, I encourage you to read some of the other Chapters in this series when you have more time. You can go to one of the other chapters by clicking on one of the buttons at the bottom. As a further inducement to keep reading, the image below gives you a simplified/approximate look at the returns (gains) you can get from these different investments.

__________________________

1 I am NOT an investment professional -- I'm an aerospace engineer with a Master's from Caltech who drifted to the business side and spent the last half of my 30-year career dealing mostly with financial matters (see Résumé). After retiring I've spent the last 25+ years investing in stocks, bonds and real estate. Although this was first updated in October 2019, I've been reviewing it regularly and make changes/additions when warranted. The views expressed here are mine and at times may depart from the norm. In preparing this article I first read several articles, and ideas or phrases from those articles may have unintentionally crept into mine; I am happy to remove any plagiarism if alerted.2 This is better than any investment, as you can read here.

3 Building a solid financial foundation before you put money into the market is important. The Emergency Fund covers essential living expenses (rent/mortgage, utilities, food, insurance). For households with two stable, secure incomes, 3 months of expenses is recommended. For single-income households, self-employed individuals, or those in less stable industries, 6 months of expenses is recommended.

4 The tax advantage comes from not having to pay taxes on the gains until you finally sell your stocks to take the money out. On CDs, you pay taxes on the gains each time a CD matures and you redeem it, so, if you set money aside from the proceeds to pay the tax, the amount that you can re-invest in another CD is NOT the whole gain from the CD you just redeemed but the after-tax amount. In a long-term investment in an S&P 500 index mutual fund, you pay taxes only when you finally sell your investment to take the money out, in 10, 20 or 30 years, so the whole gain from each year remains invested -- and gaining -- thereafter.

5 Over the 10-year period ending in June 2019 92% of stock mutual funds managed by experts did worse than the S&P 500 index stock market recommendation in these Chapters. In 2007 Warren Buffett, the 90-year-old Chairman and CEO of Berkshire Hathaway considered to be the most successful investor in history, waged a million dollars that over a 10-year period his choice of the S&P 500 index would beat the performance of top hedge funds typically seen as exclusive options for the ultra-rich -- he won handily (details here).

6 An analysis done from 1930 to 2021 showed that a person just missing the 10 best market days of each decade resulted in a total return (not annual) of 28% for the 91-year period, versus a return of 17,715% if the person had stayed invested (more here). And it's one reason for the catchy phrase "time in the market beats timing the market".

7 Historically, bonds were deemed less risky than stocks. A portfolio of both was recommended for diversification, in part because there was little correlation between them, so typically when stocks went down bonds went up and vice versa. More recently that has changed, and for beginners who have money they won't need for 5 - 10 years I recommend ONLY the two S&P 500 investments mentioned above.