This Chapter 5 is the final chapter on this series. It's intended for someone who has read Chapter 1 and perhaps some of the other detailed chapters on stocks, bonds and real estate. It covers some parting thoughts but then takes you by the hand to start investing, using what you've learned from the previous chapters. A glossary of investment terms is here.

At the end of this page, after covering various types of investments, I again raise the issue of DIVERSIFICATION.

We've touched the theme briefly, like not buying 1 or 2 stocks, and instead buying dozens or hundreds through a mutual fund. But diversification means more. It means not owning only stocks or only bonds or only real estate. It means owning some or all of them, with you deciding how much of each, depending on your goals and your comfort level with each.

Why? Because each of these investments behaves differently, and owning some or all of them reduces volatility. When there are dark economic clouds in the horizon, and the stock market goes down, bonds have historically gone up as investors look for safe places to park the funds they took out of the market (although this has shifted after 2024). And real estate, where values are typically steadier, further moderates the volatility of the entire portfolio.

If you’re younger, you can withstand more risk in your portfolio than if you’re 5 years away from planned retirement. Therefore, diversity will depend upon the markets, your age, your risk appetite, your need for income and other factors. If the amount of money you have for investing is large – say, millions of dollars – then you should diversify even beyond the United States. Some analysts believe that because of growth opportunities in other countries, such as India, investments in companies there offer greater potential for profits (along, of course, with greater risk).

The money you invest and the money that you could lose is yours. Don’t be overly influenced by others (including me!). Invest for the long haul. Investing can be risky – that’s how money is made. However, by educating yourself you’ll find that investing isn’t all that scary and you can minimize the risks, so you get a good night’s sleep every night.

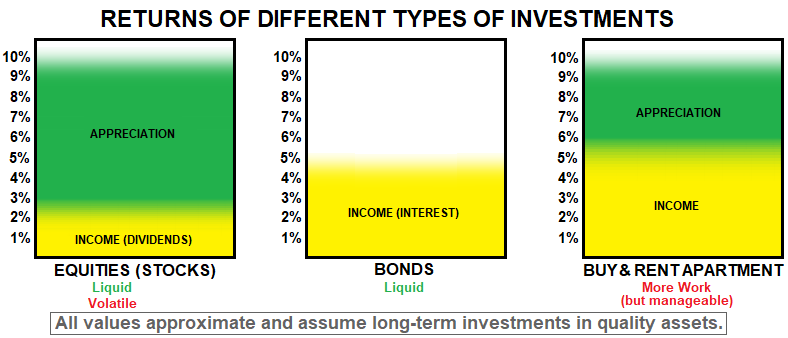

OK, let's go invest. As mentioned before, you’ve paid off all your credit cards and put away a tidy rainy-day sum. First, figure out your objectives. Looking more for income or for growth? What's your apetite for risk? How comfortable are you with buying an apartment or duplex to rent? The figure below depicts, in a simplified way, the 3 main investment options covered in prior chapters. Buying an apartment to rent out can have greater return with less volatility than stocks, but is illiquid (taking months to sell) and requires more work than just calling your stock broker (but there are techniques that minimize the hassles of being a landlord to the point where they can become insignificant; more here).

Second, based on your age and the objectives we just covered, and to make sure you're diversified, how much do you want to put in each class of investment? If you have significant funds to invest, you may choose to put 60% in stocks, 10% in bonds and 30% in real estate. If you've got a weak stomach for the volatility of the stock market, maybe 40% in stocks with the remainder split between bonds and real estate may be better. You decide. Also, every year or two after you start investing, rebalance your holdings, meaning that if your original mix was 60% stocks, 10% bonds and 30% real estate, and one of those classes has climbed a lot, so that the mix is now way off your initial target, you should sell some of the appreciated class and invest the proceeds in the other classes.

Third, let's tackle stocks. Here the decision is easy if you take my advice: put all of the amount destined for stocks in the two S&P 500 index mutual funds. But for more aggressive or more conservative investors there are other options covered in Chapter 2, so you might want to go read that again and see if maybe you want to put most in the S&P 500 index mutual funds and a bit on one or more of the other options.

Fourth is bonds. Whatever amount you choose to invest, go with high-quality/investment-grade bonds (rated BBB or above), with income of about 5%, and split the amount destined for bonds among 5 - 10 different bonds, preferably in different industries (for instance, a technology company, a health-care company and an insurance company). If you're in a high tax bracket, consider tax-free municipal bonds; again high-quality/investment-grade bonds and desirably insured.

Finally, real estate. If you want simple, or the funds you have are limited, maybe consider a real-estate mutual fund or a REIT, as discussed at the end of Chapter 4. But if you have more funds -- hundreds of thousands of dollars -- take my advice and consider buying one or more condo apartments or duplexes to rent. You need to start by deciding whether you want both income and appreciation (where you buy with cash) or only appreciation (where you get a mortgage). Then, to find the right properties, get help from a Realtor that is familiar with investment properties and will listen to your requirements. Look for condos in the $200,000 - $350,000 price range or duplexes in the $400,000 - $550,000 price range (in 2022+ $300,000 - $450,000 for condos and $550,00 - $700,000 for duplexes), in good neighborhoods (for appreciation, so it attracts good tenants and to reduce vacancy), and pick those which, if bought for cash, would have a conservative net income of at least 4% - 6% of the purchase price. You can determine that easily by going here, where I take you by the hand to help you pick and analyze properties.

The previous chapters can be accessed by clicking on the buttons below, if you need to go back. I hope you enjoyed these pages, and that they were helpful.

__________________________

1 I am NOT an investment professional -- I'm an aerospace engineer with a Master's from Caltech who drifted to the business side and spent the last half of my 30-year career dealing mostly with financial matters (see Résumé). After retiring I've spent the last 20+ years investing in stocks, bonds and real estate. Although this was first updated in October 2019, I've been reviewing it regularly and make changes/additions when warranted. The views expressed here are mine and at times may depart from the norm. In preparing this article I first read several articles, and ideas or phrases from those articles may have unintentionally crept into mine; I am happy to remove any plagiarism if alerted.