This is Chapter/Lesson 4 covering Real Estate. If your initial reaction is to skip this chapter, please don't -- real estate can work well for those looking for income and those looking for growth. Like all the chapters, this is easy reading, intended for someone who has had little if any investment experience, and only takes a few minutes. When you've read the 5 chapters, you'll be ready to invest. To start at the beginning, please go here. A glossary of investment terms is here.

There are simple and convenient ways of doing this, like real estate mutual funds or Real Estate Investment Trusts, covered later.

But I want to focus on investments which you might initially think are too much trouble but can be virtually hassle free: purchasing one or more apartments or duplexes and renting them. I cover this because these investments can deliver superior results. Depending on how they're structured, they can achieve more income than bonds plus, unlike bonds, the investment can also grow in value as the real estate appreciates. And if the investment is structured for growth, it can perform better than stocks with significantly less volatility.

Regarding my claim that this investment can be virtually hassle free, you can read more on that here.

Real Estate Purchased in Cash Principally for Income

If your interest is only in growth, skip this part and go to the next heading on this page.

The analysis that follows is intended for a person who has considered bonds and is looking for income. This works well for someone with considerable cash, perhaps a person who gets a sizeable amount of money from a divorce, or from the sale of a residence, and can pay cash for the property (why pay 5% - 6% to the bank for a mortgage on an investment property?).

In a recent analysis I compared $1 Million invested in high-quality (i.e., investment-grade) corporate bonds against the cash purchase of five $200,000 2-bedroom/2-bath condominiums for rental in the Miami area. (If you've got less cash, you can use these results by adjusting them downwards; so if you have $400,000, you'll be buying two of these condominiums, and your income and appreciation will be 40% of the numbers shown here.)

An analysis can be done where you purchase duplexes, and the results are similar to those shown here. In Chapter 5, where we actually run some examples, we'll go through the numbers for BOTH a condo and a duplex.

I selected $200,000 condos because I've found that somewhere in the $200,000 to $250,000 range for condos and $350,000 - $500,000 range for duplexes is the sweet spot for good returns without excessive hassles; more on that here).

The results of the comparison between the bonds and the 5 condominiums were that the 5 condos delivered a bit more monthly income than the bonds ($4,750 vs $4,600) after allowing for condominium expenses such as maintenance fees, property taxes and repairs, and for vacancies (details here). But there are two very important differences: the real estate delivers nearly 28% more after-tax income compared to bonds, and significant appreciation, with the real estate expected to grow to between $1.64 Million and $2.8 Million at 20 years, compared to bonds where the $1 Million didn't grow (details and total returns here).

Make sure you read the next Chapter, entitled Go Invest, where I take you by the hand and help you find the right properties to buy. Also, if you choose to skip the next section (purchasing with a mortgage), be sure to read the section after that, with comments on any real estate investments, including some of the downsides and ways of mitigating them.

Real Estate Purchased With a Mortgage for Growth

The analysis that follows is intended for someone who is looking for growth rather than income, and is considering investing in an apartment to rent out. In this case we'll be looking at financing part of the purchase with a mortgage. This works well for someone who has limited cash and also for an investor with cash who wants to use leverage to maximize returns (more on this later).

Here I looked at buying a $200,000 2-bedroom/2-bath condominium2 for rental in the Miami area with a $50,000 down payment and a $150,000 30-year mortgage of about 5.5% interest (lenders typically require greater down payment and interest for investment property, compared to an owner-occupied property).

An analysis can be done where you purchase duplexes, and the results are similar to those shown here. In Chapter 5, where we actually run some examples, we'll go through the numbers for BOTH a condo and a duplex.

The resulting monthly income would be $950 after allowing for condominium expenses such as maintenance fees, property taxes and repairs, and for vacancies (details here) but before the mortgage payment and the insurance required by the lender. When the mortgage and insurance are considered, you have zero cash flow (i.e., net income and all costs balance out); for the calculations and further details please go here.

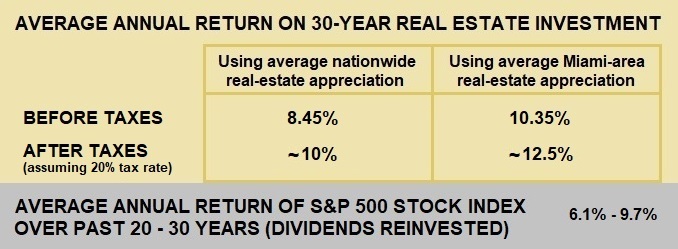

However, your gains over time are considerable because of the appreciation of the property, and it's forecast to deliver an annual return between 8.45% and 10.35% on your investment over the 30-year period of the mortgage. That's comparable or better than the S&P 500 stock market index, which has had an average annual return of 6.1% over the past 20 years, and 9.7% over the past 30 years (details here). This is partly because you're leveraging the lender's money, namely that your property -- all of your property, initially $200,000 but increasing with time -- is appreciating but you only invested $50,000.

An additional advantage of this real-estate investment, which has a bearing on your return, is that it's likely to reduce your taxes on other income. Typically, when you add the depreciation of the property (the reduction that is allowed for tax purposes in the value of an asset with the passage of time, even though the property is appreciating) to your related expenses (including mortgage interest), the investment shows in your annual income taxes as a large loss, thereby reducing the total income for the year -- in effect shielding some of the income from other sources, like your salary. So, considering this end-of-year tax savings, the above returns (8.45% - 10.35%) are comparable to a roughly 10% - 12% return from investments where the gains are taxable (income from corporate bonds are fully taxable, stock gains are taxable at a 20% rate if held over a year).

In short, for this example, the apartment-for-rent investment is comparable or superior to an investment in an S&P 500 stock market index mutual fund, and significantly superior on an after-tax basis, with less volatility. I have been too lazy to analyze the return at the 10 and 20 year points, before the mortgage is paid off, but I expect that the results will be similar. The returns presented above are in table format below. Although I stand by it, at least one person finds fault with my comparison of this real-estate investment with an S&P 500 stock investment (details here).

It's important that you read the next section, with comments on real estate investments, including some of the downsides and ways of mitigating them. Also, make sure you read the next Chapter, entitled Go Invest, where I take you by the hand and help you find the right properties to buy.

Additional Must Read Information About Real Estate Investment

Obviously, this requires more work than picking up the phone and telling your investment broker to buy a mutual fund or bonds, but as you've seen it is very rewarding, with returns that are typically superior to stocks or bonds, and without the volatility of stocks. You do need some guidance about real estate, including the areas were appreciation is likely to occur and the expected rent for a unit, but you can get such guidance from a Realtor and from the next Chapter, where I take you by the hand and help you find the right properties to buy. Also, there are techniques that minimize the hassles of being a landlord to the point where they can become insignificant; they are covered here.

To be fair, the real-estate examples presented above falls short of the so-called 1% Rule that experts recommend; the rule and why I don't adhere to it are covered here.

There is a new way to invest anywhere in the country with an online service (www.roofstock.com) that requires little effort by you. You select from properties that have been ranked for location, condition, income and tenant history, and they take care of everything, including finding you a company that will manage the property for you.

One important point is that this type of real estate investment has less liquidity; unlike stocks and bonds, if you need to cash out, it might take months to sell a property. For the average person, there are other more liquid ways of investing in real estate, such as a mutual fund that invests in real estate or a Real Estate Investment Trust (REIT) which owns real estate. I have little experience with them, but a good article on REITs and other forms of investing in real estate may be found here.

Please click on one of the buttons below to go to one of the other chapters on Investing. If you're considering buying real investment for investment, make sure you read the next Chapter, entitled Go Invest, where I take you by the hand and help you find the right properties to buy.

__________________________

1 This was updated in Oct. 2019. The views expressed here are mine and at times may depart from the norm. In preparing this article I first read several articles, and ideas or phrases from those articles may have unintentionally crept into mine; I am happy to remove any plagiarism if alerted.2 As mentioned earlier, I chose a $200,000 condo because I've found that somewhere in the $200,000 to $250,000 range is the sweet spot for good returns without excessive hassles; more on that here).